- India,

- 16-Jul-2026 03:44 PM IST

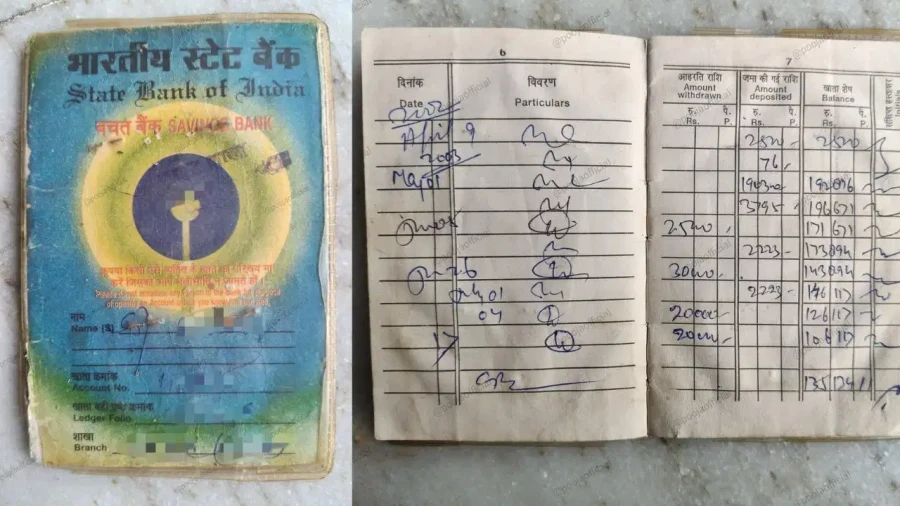

Cleaning one's home is often a journey through time, where one might encounter old photographs, forgotten coins, or various relics of the past. However, a recent discovery made by a family during a routine cleaning session has become a major talking point on social media. A young man happened to find a bank passbook that had been tucked away and forgotten for nearly two decades. This wasn't just any document; it was a State Bank of India (SBI) passbook belonging to his late grandfather, containing a significant sum of money that the family had no knowledge of for years.

The Discovery and Social Media Buzz

The incident came to light when a woman named Pooja shared the story on the social media platform X, formerly known as Twitter. She posted a picture of the old, weathered passbook, explaining how the discovery was made. The young man found the passbook while cleaning the house and immediately brought it to his father's attention. It was then realized that the account belonged to the grandfather, who had passed away a long time ago, while the family had completely forgotten about the existence of this account, and the passbook had remained hidden for about 20 to 25 years.

The Shocking Balance and Historical Value

The most startling part of the discovery was the balance recorded in the passbook. Upon checking the entries, the family found that there was more than 100000 rupees deposited in the account. To put this into perspective, the value of 100000 rupees two decades ago was substantially higher than it's today. For the family, finding this passbook was akin to discovering a hidden treasure. The revelation sparked a mix of excitement and confusion, as they were unsure about the status of the money after such a long period of inactivity.

Is the Money Lost Forever?

Given that the account holder is deceased and the account has been dormant for over 20 years, the family was naturally concerned about whether the money was still available or if it had been forfeited. Pooja's post on social media was an appeal for help, asking if it was still possible to withdraw the funds or if the money had been lost to the banking system. This query prompted a wave of responses from users familiar with banking regulations and RBI guidelines who provided clarity on the situation.

Understanding the RBI Rules for Unclaimed Deposits

According to the regulations set by the Reserve Bank of India (RBI), money lying in inactive bank accounts doesn't simply disappear. If an account remains inoperative for a period of 10 years or more, the balance is classified as an unclaimed deposit. These funds are then transferred to the Depositor Education and Awareness Fund (DEAF) maintained by the RBI. However, the crucial point is that this money remains claimable by the original depositor or their legal heirs at any time, provided they follow the correct legal and banking procedures.

The Step-by-Step Process to Claim the Funds

For the family to retrieve the 100000 rupees from the grandfather's SBI account, they must follow a specific protocol. The first step is to visit the main branch of the State Bank of India where the account was held. They will need to present the original passbook and initiate a claim for the unclaimed deposit, while the bank will then verify the details and guide them through the necessary paperwork required for such old accounts.

Essential Documentation for the Claim

To successfully claim the money, the legal heirs must provide several key documents. These include the Death Certificate of the original account holder (the grandfather), a Legal Heir Certificate to prove the relationship and right to the funds, and the claimant's own identity and address proofs. If the grandfather had registered a nominee for the account, the process becomes Importantly simpler, as the nominee can claim the funds with minimal hurdles. However, in the absence of a nominee, the bank may require a Succession Certificate issued by a court to establish the rightful successor to the deceased person's assets. This story serves as a reminder of the importance of keeping track of financial documents and ensuring that family members are aware of bank accounts and investments.